🏡 Strategy 01: Mortgage Freedom

Pay Off Your Mortgage in 5-7 Years

Velocity banking has helped over 12,000 families become mortgage-free decades early—without earning more money or changing their lifestyle.

5-7 yrs

Average Payoff

$127K+

Avg. Interest Saved

12,000 +

Families Helped

TIME TO MORTGAGE FREEDOM

Traditional Mortgage

30 yrs

Velocity Banking

7 yrs

INTEREST SAVED

$143,739

- THE PROBLEM

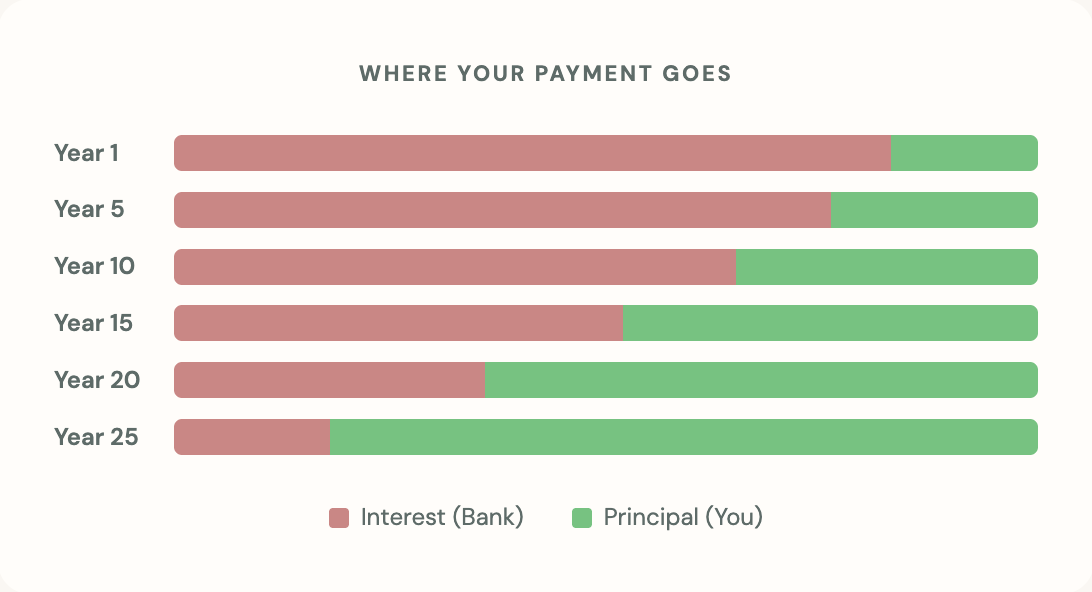

The 30-Year Mortgage Was Designed for Banks

Through "amortization," banks front-load interest payments so nearly all of your early payments go to them—not your equity.

On a $350,000 mortgage at 6.5%, you'll pay $446,247 in interest over 30 years. That's more than the house itself.

$446K

Interest on $350K Loan

83%

Year 1 → Interest

- HOW IT WORKS -

The Velocity Banking Method

A simple four-step process that uses your existing income more efficiently.

1

💳

Open a Line of Credit

Set up a HELOC or other line of credit as your "velocity account."

2

💲

Make a "Chunk"

Transfer $5K-$10K from your LOC directly to your mortgage principal.

3

🔀

Redirect Income

Deposit paychecks into the LOC. Use it for expenses. Income pays down the balance.

4

🔄

Repeat

Once your LOC is paid down, make another chunk. Each cycle accelerates payoff.

- THE MATH

Why It Works (Even If Your HELOC Rate Is Higher)

The #1 objection: "My HELOC is 8.5% and my mortgage is 6.5%—how can that save money?"

You're not comparing rates. You're comparing total interest paid.

Your mortgage charges interest on a large balance for 30 years. Your HELOC charges interest on a small, declining balance for weeks.

Because you pay down the HELOC with your entire monthly cash flow, the balance drops quickly. You never carry a large HELOC balance for long.

$446K

Interest on $350K Loan

83%

Year 1 → Interest

Example: One Chunk Cycle

DAY 1

Transfer $10,000 chunk to mortgageDAY 1

HELOC balance: $10,000 (daily interest: ~$2.33)MONTHS 1-5

$2,000/mo cash flow pays down HELOCMONTH 5

HELOC paid off. Total interest: ~$215

Interest Saved on Mortgage

$4,800+

- BENEFITS -

What Velocity Banking Gives You

📅

Guaranteed Payoff Date

Unlike market-based strategies, velocity banking is pure math. Your payoff date is predictable.

💵

Save $100K-$200K+

Eliminate years of interest payments. That money stays in your pocket for retirement or your kids' future.

⚡️

No Extra Income Needed

You're not working harder. You're using your existing income more efficiently.

🛡️

Build Equity Faster

Own more of your home sooner. More equity means more options for refinancing or selling.

🙂

Peace of Mind

Imagine life without a mortgage payment. That's freedom and security for your family.

🎓

Retire Earlier

Without a mortgage, your cost of living drops dramatically. Many clients retire 5-10 years earlier.

- Common Questions -

Is This Too Good to Be True?

Here are the questions smart people ask—and honest answers.

Q

"My HELOC rate is higher than my mortgage!"

You're comparing rates, not total interest. Your mortgage charges interest on a huge balance for 30 years. Your HELOC charges interest on a small, rapidly-declining balance for weeks. The math works in your favor.

Q

"Why haven't I heard of this before?"

Banks profit from 30-year mortgages. Financial advisors profit from investments. Neither has incentive to teach you this. Wealthy families have used this for generations—it's just not advertised.

Q

"Isn't this risky?"

It requires discipline, not risk-taking. You're actually safer—you build equity faster, giving you more options if life throws a curveball. The main "risk" is overspending on your LOC.

Q

"I don't have a HELOC—can I still do this?"

A HELOC is ideal but not required. Personal lines of credit and even 0% intro APR cards can work for smaller chunks. We can help you identify the best tool for your situation.

"Peter showed us how to pay off our mortgage 18 years early. We're saving over $140,000 in interest—money that's now going toward our retirement. I wish we had found this strategy 10 years ago."

Sarah M.

Texas • Velocity Banking Client

See Your Personal Numbers

Use our free calculator to see exactly how fast you could pay off your mortgage.

- go deeper -

Learn More About Velocity Banking

Ready to Become Mortgage-Free?

Take our 2-minute assessment to see if velocity banking is right for you—and get your personalized payoff timeline.

✓ 2 minutes • No commitment • Personalized results

Helping families build wealth through guaranteed strategies—because your financial future deserves certainty, not chance.

"Guarantees Over Gambles."